Dow Theory Swing Trade Type EA Selene] Won a prize at the FXGT trading competition!

A collection of several financial instruments held by an investor. Balanced diversification across a range of assets, such as stocks, currencies and commodities, can improve investment efficiency and diversify risk.

It is also possible to diversify the timing of trades by adopting several different trading strategies within the same stock or by diversifying time frames, thereby reducing the impact of single risks.

It is important to strike a balance between operational efficiency and risk in investments. Investment efficiency indicates how effectively the return earned on an investment can be increased in relation to the risks associated with the investment. Generally, the higher the return, the higher the risk, so operational efficiency depends on how much risk you are willing to accept.

Increasing investment efficiency may result in higher returns, but at the same time increases risk, so care must be taken. Conversely, minimising risk as much as possible will ensure safety, but will also result in lower returns. Investors should optimise the balance between investment efficiency and risk according to their own risk tolerance.

Optimal portfolio selection is the construction of a portfolio that best suits the investor's objectives, taking into account the balance between investment efficiency and risk. The concept of optimal portfolio selection includes the following elements.

First, it is important to define your investment goals and set your risk tolerance. Investment goals should be specific and achievable, such as increasing assets, securing income or securing retirement living costs. Risk tolerance indicates the level of risk an investor is willing to accept and is determined by taking into account factors such as age, asset situation and investment period.

The next step is to determine the optimal asset allocation. Asset allocation determines the proportion of assets in a portfolio and is an important factor in optimising the balance between risk and return. Asset allocation adjusts the proportions of asset classes such as equities, bonds and property according to the investor's risk tolerance and investment objectives.

Finally, risk diversification is achieved by selecting appropriate stocks for each asset class. Stock selection can be done through fundamental or technical analysis. Diversification by sector and region can further reduce risk.

Optimal portfolio selection ensures that the balance between investment efficiency and risk is optimised and that the portfolio management meets the investor's objectives. It is therefore important for investors to carefully select portfolios according to their objectives and risk tolerance.

One of the main attractions of using MT5 is the ability to utilise automated trading systems (Expert Advisors: EAs), which are programs with trading rules and conditions that allow automated trading. As trades can be automated for a wide range of investment patterns, efficient portfolio management is possible by trading without the influence of time constraints and emotions.

MT5 allows you to create your own EAs or buy and use EAs developed by other traders. This allows automated trading to be executed based on your own strategy, so that you can tailor it to your individual investment objectives.  Forex Automated Trading Tool [Dow Theory Swing Trade Type EA Selene] Product OverviewProduct Overview Sequential swing trade type EA based on Dow Theory The Dow Theory Indicator will make entries in the forward direction at points judged to be favorable for entry b

Forex Automated Trading Tool [Dow Theory Swing Trade Type EA Selene] Product OverviewProduct Overview Sequential swing trade type EA based on Dow Theory The Dow Theory Indicator will make entries in the forward direction at points judged to be favorable for entry b

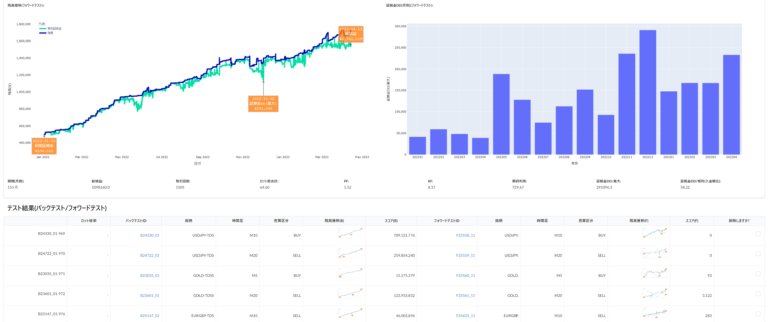

The standard MT5 functionality allows you to run back/forward tests of individual EAs and check the results,

However, it is not possible to synthesise the test results of multiple EAs and generate a single operational result.

To address this issue, we have built our own management system and developed a report function that can combine backtest results.

※Currently, it is possible to generate reports by combining test results from only the EAs published on this website.

Portfolioing and reporting including the test results of external EAs is not currently supported, but if there is a need, we will consider putting this into place.

High-profile brokers such as XM and HFM offer a very wide range of stocks.

Not only currency, but also commodities such as GOLD, stock indices such as SP500 and NASDAQ futures, and crypto assets such as Bitcoin can be managed.

In particular, HFM also handles individual stock issues and ETFs, and has a very wide range of potential issues, so there is no shortage of investment options.

By using MT5 in combination with an overseas brokerage firm, you can obtain an environment that allows you to perform automated trading on a wide range of stocks,

If you select EAs that can be operated stably and build a portfolio combining EAs, there is no doubt that your win rate will increase.

Backtesting is a method of using historical data to verify how effective current investment strategies have been.The MT5 platform can be used to run backtests on automated trading systems and investment strategies. Based on historical market data, you can see how your portfolio has performed under different scenarios. However, care should be taken not to rely too heavily on backtesting results, as results based on historical data do not necessarily guarantee future outcomes.

It is important to forward test portfolios created using back-test results to ensure that they are not over-optimised (curve-fitting) to the back-test results.

The optimisation of an EA starts with optimising against historical data for the back-testing period,

Therefore, forward testing over a period of time that does not include this period can be used to check for generalisation performance.

Example: if the back-testing period is from 01/01/2008 to 31/12/2021, the forward test should be from 01/01/2022 to the previous day's date.

There are no clear rules on the ratio between the length of the backtesting and forward testing periods,

As a general rule, a ratio of 7:3 or 8:2 is desirable.

However, if the number of trades during the backtesting period cannot be secured to a certain extent, the quality of the backtesting itself becomes questionable, and the period of historical data that can be prepared for each stock should also be comprehensively considered and the period adjusted.

When assessing investment performance, it is important to select an appropriate index as a benchmark. Benchmarks provide a basis for comparing the performance of one's portfolio with other investors and investment products. Typically, major stock indices (e.g. S&P 500, Nikkei 225) are used as benchmarks for equity investments and bond indices (e.g. Barclays US Aggregate Bond Index) for bond investments.

Comparison of the benchmark and the portfolio's rate of return can be used to judge the quality of investment performance. If the portfolio's rate of return is above the benchmark, the investment strategy is successful. Conversely, if it is below the benchmark, the investment strategy needs to be reviewed.

The Sharpe and Soltino ratios are measures of the risk-adjusted return of an investment portfolio. The Sharpe ratio is calculated by dividing the portfolio's rate of return minus the risk-free interest rate by the portfolio's standard deviation (risk). The higher the value, the higher the return on risk taken is assessed.

The solvino ratio, on the other hand, is calculated by dividing the portfolio's rate of return minus the risk-free interest rate by the portfolio's risk of decline (bad risk). Here too, a higher value is rated as a higher return on risk taking, but differs from the Sharpe ratio in that it focuses only on downside risk.

Regularly reviewing your portfolio is important in order to adapt to changes in the investment environment and markets. For example, analyse your portfolio at regular intervals, such as once a year or once every six months, and re-evaluate your asset allocation and investment stocks. During the review, it is important to consider the balance between risk and return of the portfolio and to pursue investment efficiency in line with your goals. Regular reviews can optimise your portfolio, thereby improving investment efficiency while reducing risk.

We have introduced the basic concept of the portfolio.

We are planning to gradually expand the number of EA strategies and stocks managed on this website, so we hope that you will consider portfolioisation as well and make use of it to formulate a stable investment policy.

We will also be brushing up the functions and indicators related to portfolioisation so that we can propose more transparent strategies, so please make use of these reports.